Every shopper wants to find a bargain; it’s one of the thrills we get when we go to buy something. Finding what we want at a lower price than we had planned to spend is always exciting. And this is also true for the stock markets. It’s the appeal of value stocks.

According to Bank of America, the value stock segment, which typically trades below what their underlying strengths suggest, has lagged growth stocks significantly so far this year. Savita Subramanian, a quantitative and equity research strategist at the bank, describes value stocks as “neglected and trading at very low multiples” and points to several sectors, including energy stocks, as a place where value-minded investors can look for opportunities.

Subramanian’s colleague, Bank of America equity analyst Kalei Akamine, has taken that stance and has taken a deep dive into three value-priced energy stocks. All three are members of the S&P 500 value index, and in Bank of America’s view, these are value stocks to watch right now.

According to TipRanks database, Wall Street’s overall opinion on these options is clear: they have a buy rating and offer solid double-digit growth potential. Let’s look at the details and find out why Bank of America thinks they are attractive options for the portfolio.

ConocoPhillips (POLICE)

We’ll start with ConocoPhillips, one of the world’s largest independent oil and gas exploration and production companies. With a market capitalization of $131 billion, ConocoPhillips oversees a global operation from its headquarters in Houston, Texas; the company has activities in North America, Europe, Africa, the Middle East, and the Asia-Pacific region.

Zooming out, ConocoPhillips is deeply involved in the production of most forms of fossil fuel. The company’s operations include all phases of discovery, exploitation, transportation and distribution/marketing of hydrocarbon fuels and other products, including crude oil, natural gas, natural gas liquids, liquefied natural gas (LNG) and bitumen, also known as natural asphalt. ConocoPhillips maintained an average daily production last year of 1.826 billion barrels of oil equivalent and, as of December 31, claims to have approximately 6.8 billion barrels of oil equivalent of proven reserves on its properties and operating areas. The company’s largest crude oil and natural gas production region was the “contiguous 48 states” of the United States.

For investors seeking returns, this company maintains a strong commitment to returning capital to shareholders. In 2023, the company returned $11 billion to its shareholders, in compliance with its policy of returning more than 30% of its cash from operations.

In the most recently reported quarter, 1Q24, ConocoPhillips had sales and operating income of $14.5 billion. This was more than $480 million lower than expected and was based on total quarterly production of 1,902 Mboe/d. The company’s bottom line was $2.03 per share on a non-GAAP basis, in line with expectations.

The US oil and gas sector has seen several high-profile M&As over the past year, and BofA analyst Akamine believes this is positive for ConocoPhillips. He writes: “We believe the current M&A cycle has reshaped the competitive landscape in US E&P to the benefit of names with size and growth. With the acquisitions of Concho, Pioneer and Hess since the start of the decade, there is now a void for exposure to high-quality, large-cap oil. We believe that will continue to drive investors towards COP, the largest independent E&P company by production and market capitalisation…”

Laying out his long-term view on the stock, the analyst adds: “In our view, COP’s asset mix and depth of resources are the undervalued aspects of the investment case. The depth of the US portfolio has enabled COP to deliver category-leading visibility, with a 10-year plan targeting a 4-5% production CAGR. While that sounds modest, there is a compounding effect that generates significant cash flow growth.”

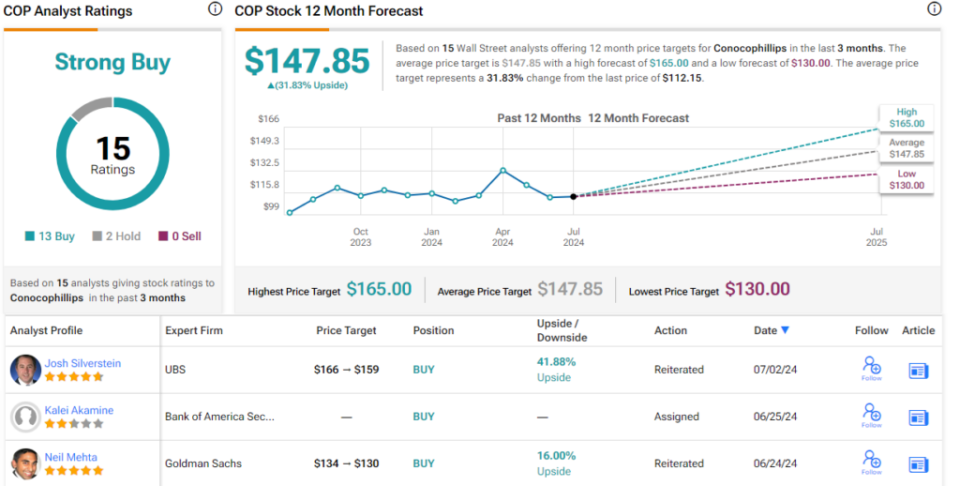

These comments support Akamine’s buy rating on the stock, and its $147 price target implies a 31% one-year upside (to watch Akamine’s track record, click here).

Overall, this oil and gas giant receives a Strong Buy consensus rating from Wall Street, based on 15 recent reviews that include 13 Buys versus just 2 Holds. Shares are priced at $112.15, and the average price target of $147.85 is only marginally more bullish than BofA’s estimate. (See ConocoPhillips Stock Forecast.)

Devon Energy (DVN)

Next up is Devon Energy, an independent exploration and production company based in Oklahoma. Devon focuses its activities on the extraction of recoverable energy products from onshore assets located in the continental United States. The company operates in five states (Texas, New Mexico, Oklahoma, Wyoming and North Dakota) and is active in some of the richest energy regions in the country, including the Williston Basin, Delaware Basin and Eagle Ford Formation.

Devon, a $30 billion company, has worked to develop a stable asset portfolio designed to promote strong future production growth while operating in an environmentally responsible manner. The company generated strong production figures during the first quarter of this year, recording average daily production of 319,000 barrels of oil, 165,000 barrels of natural gas liquids and 1 billion cubic feet of natural gas. In total, this amounted to 664,000 barrels of oil equivalent per day, exceeding previously released guidance by 4%.

The production generated total revenue of $3.6 billion, down 5.8% from the same period last year but in line with forecasts, while net earnings per share (EPS) of $1.16 on a non-GAAP basis was five cents above estimates. The company ended the first quarter with $1.15 billion in cash on hand, a solid increase from $887 million reported in Q1 2023 and $875 million reported in Q4 2023.

Checking in with analyst Akamine, we find that the BofA energy expert is bullish on Devon, citing that looking ahead, the company is poised to outperform. Akamine writes, “Our Buy rating on DVN reflects a turnaround story centered on DVN refocusing its drilling program on its best assets in the Delaware of New Mexico, and looking to reestablish itself as one of the premier operators in the sector… With initial 2024 guidance set in the wake of a challenging quarter in Q3 2023, we believe DVN has reestablished the path to ‘outperform and up. ’ In its Q1 2024 results, DVN raised fiscal 2024 oil guidance, attributing strong well performance in the Permian, and appears to have regained some of that operational momentum.” Through the end of 2024, we expect to see Permian oil stabilize around 212 mbd, which could set the stage for strong guidance for fiscal 2025.”

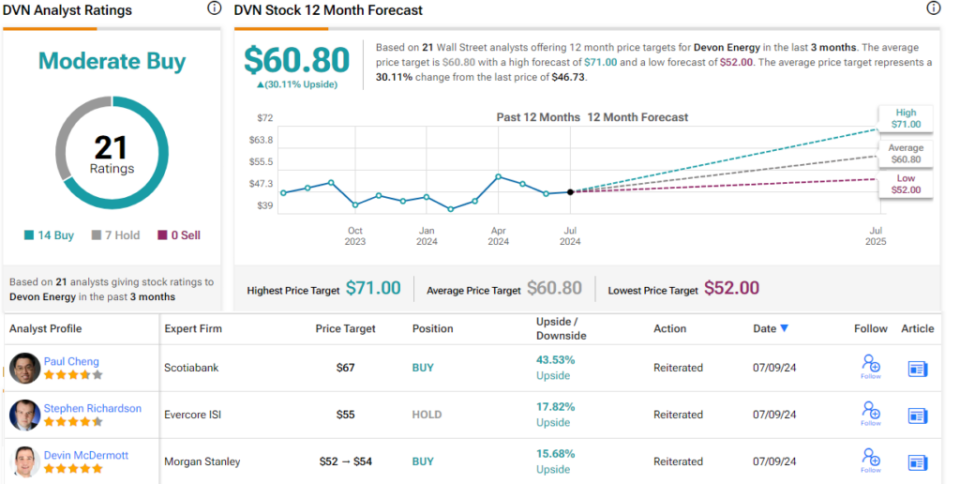

Along with his Buy rating, the analyst sets a $64 price target here, suggesting 37% upside potential over the next 12 months.

Devon Energy has been given a Moderate Buy rating by the Wall Street consensus, based on 20 recommendations that break down into 14 Buys and 7 Holds. The stock is priced at $46.73 with an average price target of $60.80, indicating a one-year upside potential of 30%. (See Devon Stock Forecast.)

End of degree resources (end of career)

Last on our list of BofA-backed companies is EOG Resources, another of North America’s large independent energy companies. EOG, with a market capitalization of about $72 billion, is active in the northern and southern Great Plains, as well as the Appalachian region. The company has productive oil and gas exploration and extraction operations in the Appalachian Basin, the Eagle Ford Formation, the Midland Basin, and the Permian Basin, and in the Williston, Powder River, and DJ Basins. In addition, the company has an offshore operation in the Columbus Basin, near the island nation of Trinidad and Tobago. EOG is headquartered in Houston, Texas, near the epicenter of the 21st century energy renaissance.

On the production side, EOG exceeded the midpoint of 1Q24 guidance for crude oil, natural gas liquids and natural gas, and saw modest gains over 4Q23. The company’s crude oil production in the first quarter came in at 487.4 MBbld; natural gas liquids reached 231.7 MBbld and natural gas production came in at 1.858 MMcfd. The company’s total production in the quarter, converted to crude oil equivalent volumes, was reported at 1,028.8 MBoed.

Those production numbers supported EOG’s quarterly revenue of $6.12 billion. That represented a modest 1.3% year-over-year increase, but beat forecasts by nearly $1.8 billion. The company’s net income figure of $2.82 per share on a non-GAAP basis was 24 cents per share better than expected.

Not only does this company generate solid hydrocarbon production numbers, but it also generated a lot of cash in the first quarter of 2024. EOG’s cash flow from operations was recorded at $2.9 billion. After deducting $1.7 billion in capital expenditures, the company reported $1.2 billion in free cash flow.

When we last checked in with BofA analyst Akamine, we found that he likes this company for its combination of long-term staying power and cash generation. The energy analyst says, “EOG’s portfolio supports drilling at the current pace in the Permian Basin for 19 years, twice as long as the peer average. Post-COVID, valuations have been calibrated around FCF yields, which undervalues longer-term inventory. But as the industry depletes core locations and looks to replenish through costly M&A, we see EOG increasingly better positioned and deserving of a premium multiple.”

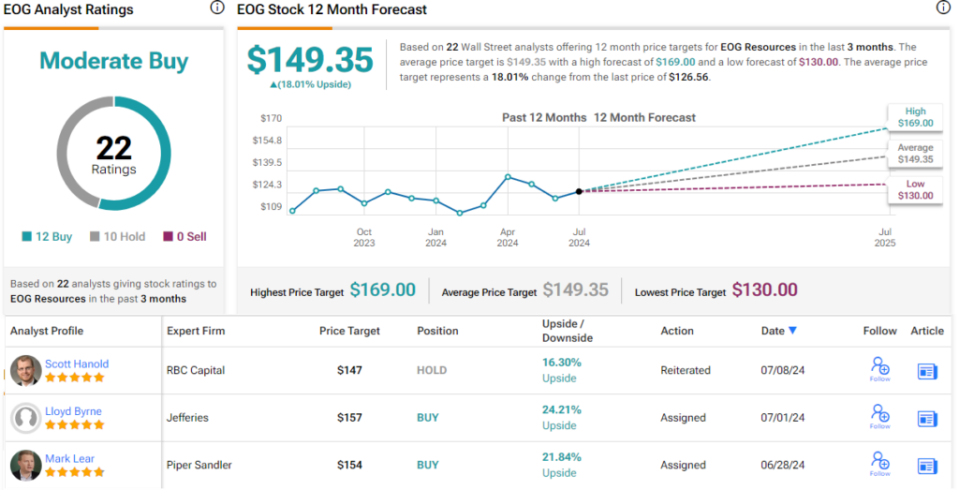

Akamine rates this stock a buy and sets a $151 price target to point to a 19.5% upside over a year. (To watch Akamine’s track record, click here.)

Overall, EOG has a Moderate Buy consensus rating, based on 22 reviews with a 12-10 breakdown favoring Buys over Holds. The stock is currently trading at $126.56 and its $149.35 average price target implies a one-year upside potential of 18%. (See EOG Stock Forecast.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks. Best Stocks to Buy, a tool that brings together all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important that you do your own analysis before making any investment.